Unlocking Sri Lanka's Digital Dollar Economy: How USDT, PFCAs, and PayPal Can Rebuild Forex Reserves

Sri Lanka's traditional forex inflow channels, tea exports, tourism, worker remittances, face structural headwinds. A decentralised, digital-first pivot through stablecoins, formal foreign currency accounts, and global payment gateways offers a new pathway to rebuild reserves and modernise the macroeconomy.

As Sri Lanka navigates its post-crisis economic recovery, the conversation in policy circles has focused heavily on the traditional pillars of foreign exchange inflow — remittances, export earnings, and tourism receipts. These sectors remain foundational. But the global economic landscape has shifted, and a new category of high-velocity, digitally-native capital inflow has emerged that Sri Lanka has yet to systematically harness.

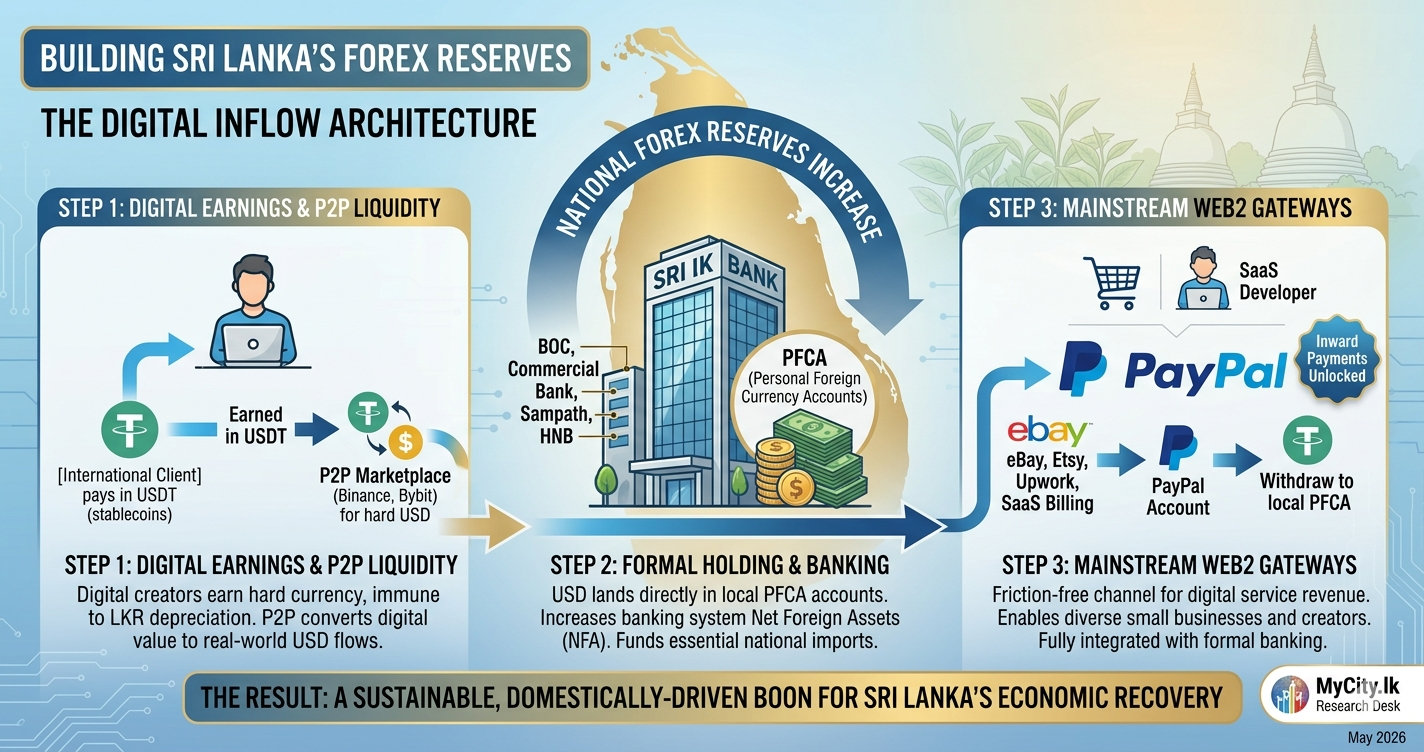

Three instruments sit at the centre of this opportunity: USDT peer-to-peer trading as a decentralised liquidity mechanism, Personal Foreign Currency Accounts (PFCAs) as the formal domestic holding infrastructure, and PayPal inward payments as the mainstream Web2 gateway for digital service revenue. Together, they form a three-layer architecture capable of funnelling significant global USD flows directly into Sri Lanka's banking system.

The USDT P2P Engine - A New Inflow Mechanism

Peer-to-peer trading of USDT has evolved from a niche crypto activity into a highly efficient cross-border settlement and arbitrage tool. For Sri Lankan digital service providers, remote developers, content creators, and day traders, earning in USDT offers something the local banking system cannot: immediate immunity from LKR depreciation and a direct connection to global dollar liquidity.

How the Arbitrage Benefit Works

When a Sri Lankan freelancer earns USDT from an international client and subsequently sells that USDT on a P2P marketplace, Binance, Bybit, or KuCoin, to a global buyer who needs digital stablecoins, the mechanics are straightforward:

Unlike traditional remittance systems that charge structural fees and convert incoming capital into LKR at fixed, unfavourable bank buy rates, P2P settlements ensure value is retained directly in hard currency. The Sri Lankan earner acts as a decentralised liquidity provider to the global stablecoin market — and gets paid in dollars that can be formally banked.

Sri Lankan digital earners avoid two costs simultaneously: the LKR depreciation risk between earning and converting, and the structural remittance fee that traditional wire services charge. USDT received from global clients and sold via P2P to international buyers results in clean USD hitting a formal banking channel — with no intermediary taking a percentage.

PFCAs - The Formal Holding Infrastructure

Bringing foreign currency into the country is only half the equation. Keeping it securely within the domestic banking ecosystem is what structurally moves the needle for national reserves. This is where Personal Foreign Currency Accounts (PFCAs) become the critical infrastructure layer of this entire framework.

When P2P earnings or freelance digital payouts are routed via SWIFT directly into a local PFCA at Bank of Ceylon, Commercial Bank, Sampath Bank, or HNB, the cascading macroeconomic benefits are substantial:

Shores Up Central Bank Reserves

Hard currency in local commercial bank PFCAs improves the banking sector's overall net foreign assets (NFA), giving banks liquidity to fund crucial national imports.

Incentivises the Depositor

PFCAs allow citizens to legally hold funds in USD at competitive interest rates, paid in foreign currency — completely removing the immediate compulsion to convert to a depreciating LKR.

Formalises Capital

Moving P2P earnings into official PFCAs shifts transactions out of underground Undiyal/Hawala networks and places them within the verified, audited banking system — enhancing AML compliance.

Tax Visibility

Formalised digital earnings become visible to the Inland Revenue Department, creating a sustainable tax base from the emerging digital economy rather than losing it entirely to informal channels.

The USDT → PFCA Pipeline — Step by Step

Formalisation PathwayEarn USDT from International Clients

Digital service providers, developers, and freelancers receive USDT directly from overseas clients to their wallet address — bypassing traditional wire transfer friction entirely.

TRC-20 · ERC-20 · BEP-20Sell USDT via P2P to International Buyers

On Binance or Bybit P2P, the Sri Lankan seller lists their USDT. An international buyer who needs stablecoins purchases them and sends USD via SWIFT to the seller's banking details.

Binance P2P · Bybit P2PUSD Arrives in Sri Lankan PFCA

The SWIFT transfer lands directly in the earner's PFCA account — legally held in USD, within the Sri Lankan banking system, without forced LKR conversion.

BOC · Commercial Bank · Sampath · HNBHard USD Strengthens National NFA

USD sitting in Sri Lankan commercial bank PFCAs contributes to the banking system's net foreign assets — improving the country's aggregate foreign currency position.

CBSL Net Foreign Assets ImprovePayPal - The Catalyst for Mainstream Digital Revenue

While USDT P2P networks offer a parallel, high-velocity lane for digital capital inflow, mainstreaming the digital economy requires integration with standard Web2 financial infrastructure, most notably, fully functional inward PayPal payments.

Sri Lanka currently has a significant restriction: citizens can use PayPal to send money abroad, but the ability to receive commercial payments is severely restricted. This single limitation acts as a bottleneck on an entire category of digital entrepreneurship.

Sri Lankan eBay sellers, Etsy artisans, independent SaaS developers, Upwork professionals, and sub-contractors for international firms cannot invoice global clients through PayPal and receive payment into Sri Lanka. Every such transaction either routes through a third country or is lost to informal channels entirely. The estimated monthly value of this blocked flow is substantial.

Unlocking full inward PayPal functionality, and structurally linking those PayPal accounts directly to local PFCAs, would create a clean, friction-free pipeline for every category of digital service revenue:

eBay & Etsy Sellers

Sri Lankan artisans and exporters who sell internationally could receive payments directly, without routing through UAE or US personal accounts.

SaaS Developers

Independent software developers billing international clients monthly could formalise revenue into PFCAs rather than losing it to informal channels.

Freelancers & Creatives

Designers, writers, marketers working for international brands on Upwork, Fiverr, and direct contracts could receive and bank income legally.

Sub-Contractors

Businesses acting as sub-contractors for international firms, in IT, manufacturing, and services, could formalise what currently flows through informal channels.

The Macro Equation - Rebuilding Forex Reserves Formulaically

The macroeconomic case for this three-layer digital economy framework can be modelled clearly. Let national incoming digital service revenue be represented as the elastic variable that policy can expand, alongside traditional inflows.

R_t = Traditional remittances (worker transfers, Migrant Worker Remittances)

R_d = Digital economy revenue, USDT P2P + PayPal + freelance PFCA inflows

Exports = Tea, garments, tourism receipts, other goods/services

Imports + Debt Service = The outflow side of the equation

The critical insight is that R_d , digital economy revenue, is uniquely elastic. Unlike physical exports that require infrastructure, logistics, and commodity price conditions, digital service revenue scales with human capital and internet connectivity. It does not require container ships, warehouses, or favorable tea auction prices.

By expanding the digital economy channel through unregulated-to-regulated hybrid pipelines, USDT → P2P → PFCA, Sri Lanka introduces a high-velocity, low-infrastructure revenue variable that can grow rapidly without the capital expenditure that traditional export growth requires.

A Progressive Regulatory Vision

For Sri Lanka to harness this opportunity, the regulatory environment must shift from institutional friction toward progressive alignment. The CBSL, in tandem with local commercial banks, must actively draft frameworks that welcome digital assets and clean P2P dollar flows into domestic PFCAs rather than treating them with blanket suspicion.

"Embracing global decentralised liquidity is not about replacing local banking infrastructure, it is about building high-speed entry ramps that funnel global USD into domestic reserves."

- The core policy reframe that shifts crypto from a threat to an asset for Sri Lanka's economic recoveryThe regulatory priorities are clear and sequenced:

Formalise USDT-to-PFCA Pipelines

Issue clear guidance recognising USDT P2P earnings as a legitimate foreign currency inflow category, allowing direct SWIFT routing into PFCAs without triggering AML flags for compliant transactions.

Unlock Full PayPal Inward Access

Negotiate with PayPal to enable inward commercial payments for Sri Lankan accounts, linked to verified PFCAs. Every PayPal payout becomes a formal USD entry into the banking system.

Incentivise PFCA Use for Digital Earners

Offer competitive USD interest rates on PFCAs specifically for digital economy earners. Remove friction in the SWIFT routing process. Make the formal channel more attractive than informal alternatives.

Treat Web3 as Raw Capital Acquisition

Reframe USDT not as a speculative asset to be restricted, but as a raw capital acquisition tool that, when properly channelled, injects hard USD into the domestic reserve base.

The CBSL has indicated that AML/CFT-focused crypto regulations are in development, with draft guidelines expected. This is the moment to shape that framework toward formalisation rather than restriction, establishing Sri Lanka as a forward-thinking jurisdiction that channels global digital liquidity into national reserves, rather than pushing it further underground.

The Path Forward - Sri Lanka as a Digital Economic Hub

By treating Web3 instruments like USDT as raw capital acquisition assets, PFCAs as national holding infrastructure, and mainstream payment rails like PayPal as the friction-free consumer layer, Sri Lanka can transition into a high-reserve digital economic hub without the heavy physical infrastructure that traditional economic development pathways require.

The talent base is already present. Sri Lanka has a technically educated workforce, a strong diaspora connected to global markets, and an existing culture of digital freelancing and remote work. What is missing is the regulatory architecture to formalise the flows these people are already generating informally.

Every Sri Lankan digital service provider routing earnings through formal PFCA channels is simultaneously strengthening their own financial position and contributing to national net foreign assets. The policy goal is not to mandate this, it is to make the formal pathway so frictionless and rewarding that it becomes the obvious choice over informal alternatives. When the formal channel wins on convenience and cost, the national reserve picture improves automatically.