Does Trading USDT in Sri Lanka Actually Take Money Out of the Country?

Most people assume peer-to-peer crypto trading drains national fiat reserves. The reality is far more nuanced, and understanding the real mechanics reveals something much bigger than a simple yes or no.

"When Sri Lankans buy and sell USDT between each other locally, does the national fiat actually leave the country, or are we just moving money between ourselves?"

It is a question that sits at the intersection of monetary economics, crypto mechanics, and developing-world financial realities. And the answer is more layered than most people expect. Let us work through it carefully.

What Actually Happens in Local P2P Trading

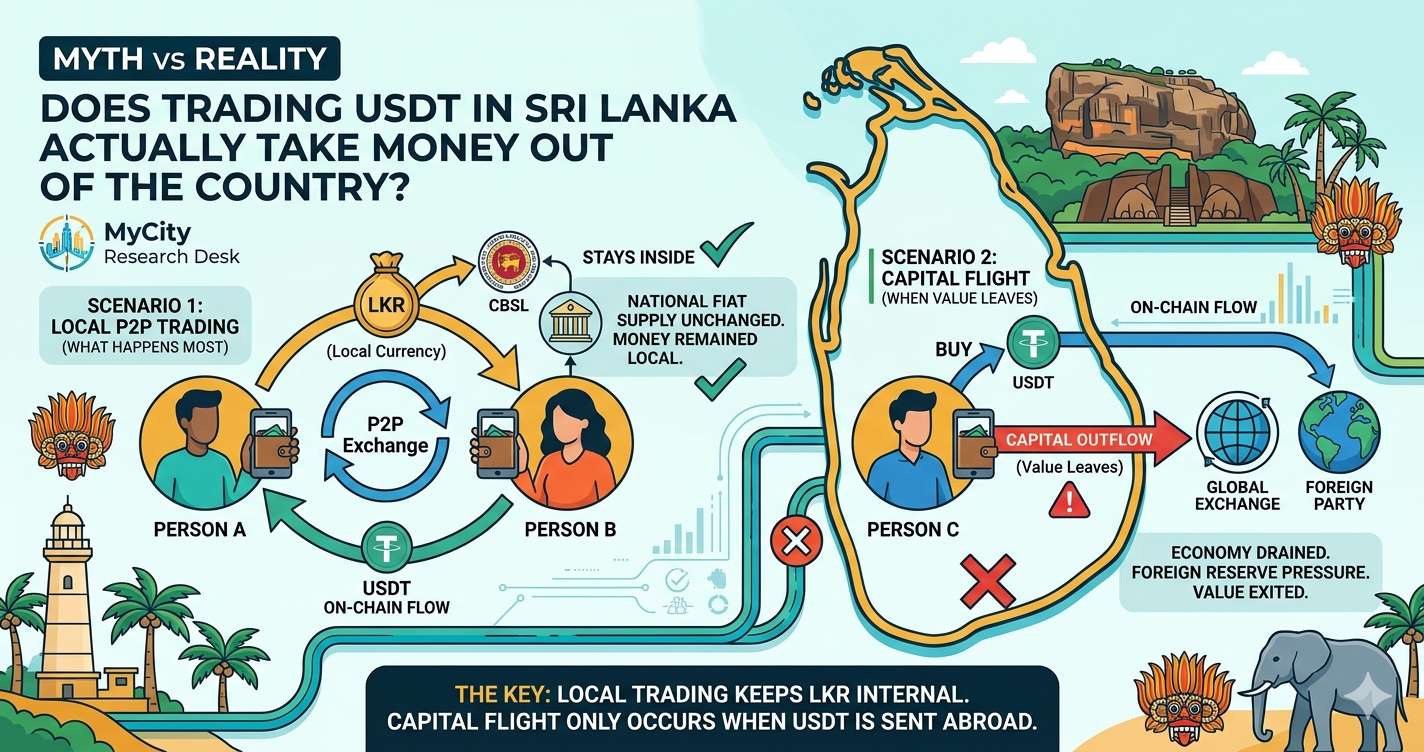

Imagine two people inside Sri Lanka. Person A has LKR sitting in a local bank account. Person B already owns USDT. Person A wants to buy 100 USDT from Person B.

This is the critical insight that most casual observers miss. The same amount of LKR still exists inside Sri Lanka. It simply moved from Person A's bank account to Person B's bank account. No USD physically entered or exited the banking system. No foreign reserve was touched.

At a pure local level, two Sri Lankans, two wallets, one trade, the national fiat supply is entirely unchanged. What changed is who holds the USDT and who holds the LKR.

This is not trivial to understand because it runs against the intuition that "buying a dollar-pegged asset means the dollar went somewhere." In a fully domestic P2P trade, it did not, not yet.

USDT as a "Layer 2" on Fiat Rails

This brings us to a framing that is increasingly being adopted by monetary economists studying developing economies, the idea of stablecoins functioning as a Layer 2 liquidity network sitting on top of fiat infrastructure.

The local banks still process deposits, withdrawals, and transfers. The national fiat system still anchors everything. But increasingly, the "store of value" and "trading asset" layer is shifting toward USDT, operating in parallel, above the fiat rails, rather than replacing them.

The analogy that captures this most cleanly is actually quite elegant, and it comes from the crypto world itself. Just as Bitcoin's Lightning Network is a "Layer 2" built on top of Bitcoin's base layer to enable faster, cheaper transactions without changing the underlying protocol, USDT is increasingly functioning as a Layer 2 on top of national fiat systems in developing economies.

When Crypto Does Affect National Currency

This is where the picture gets considerably more complex, and where the "it's just peer-to-peer, nothing leaves" argument breaks down.

A. Demand Shift Away From Fiat

Even if individual P2P trades do not immediately remove fiat from the country, the preference shift matters enormously at scale. If millions of Sri Lankans begin preferring to hold USDT over LKR as their savings vehicle, the demand for LKR decreases.

That demand shift weakens the currency's fundamentals, not through any single transaction, but through the aggregate behavioral change. This is effectively a slow, informal dollarization occurring outside the banking system's visibility.

B. Capital Flight, When Value Actually Leaves

Here is the scenario where real economic value exits the country:

Even though no physical cash crossed a border, purchasing power left. The LKR that Person A spent to buy that USDT is now in Person B's hands, but the economic value it represents has been exported as purchasing power to a foreign jurisdiction.

C. Banking Liquidity Changes

There is a third, slower mechanism that regulators are particularly concerned about. If people stop saving in banks and begin holding stablecoins instead, the banking system experiences measurable structural changes:

Fewer Deposits

Less capital sitting in bank accounts reduces the raw material banks use to make loans.

Reduced Lending Capacity

Banks with lower deposit bases lend less, constraining credit availability in the economy.

Weaker Monetary Transmission

Central bank interest rate decisions have less impact when savings bypass the banking system.

Reduced Visibility

Regulators lose sight of economic flows that move into crypto rails, complicating policy.

Why Governments Get Concerned

It is worth being precise about what governments are and are not worried about, because the popular narrative often conflates these things.

Small peer-to-peer swaps between citizens holding USDT locally. These do not directly impact national reserves or monetary supply in the short term.

Loss of monetary sovereignty. The inability to monitor economic flows. Tax leakage on unreported crypto gains. Sanctions evasion through borderless transfers. Unofficial dollarization reducing central bank control. And the gradual erosion of the fiat system's dominance in daily economic life.

Central banks operate through controlling liquidity, setting interest rates, managing banking reserves, and influencing currency demand. Stablecoins partially bypass all of those mechanisms, not by breaking them, but by routing economic activity around them.

The Casino Analogy

There is a classical economics analogy that maps almost perfectly to what is happening with USDT in economies like Sri Lanka's, and understanding it clarifies both the opportunity and the risk.

The Casino Economy Analogy

Imagine a casino operating inside a country. People exchange fiat for casino chips. Those chips circulate heavily, games, trades, bets, transfers between players. But the underlying fiat mostly remains in the casino vault system. People are operating in a secondary economy of chips that is anchored by, but somewhat detached from, the national fiat system.

USDT often works similarly. It functions as digital chips circulating faster and more freely than fiat, while fiat still anchors the entry and exit points. The critical difference: USDT is globally transferable and interoperable. Casino chips cannot leave the building. USDT can cross borders in seconds, without a central authority's permission, to anywhere on earth.

That is what makes stablecoins fundamentally different from any previous parallel currency system, and what makes the regulatory picture so genuinely complex.

The Deeper Monetary Shift Happening Globally

Stablecoins like Tether are not simply a new financial instrument. They are creating something that did not previously exist: a privately operated, internet-native dollar network that functions independently of any government's permission, infrastructure, or monetary policy.

In many developing regions, including Sri Lanka, the behavioral patterns are already shifting:

People trust USDT more than local banks for savings. Merchants informally accept it for high-value transactions. Traders price assets in it rather than local fiat. Remittances increasingly route through USDT rather than traditional wire transfers. Cross-border payments move in seconds rather than days.

Analysts describe this emerging reality using several frames, each capturing a different aspect of the same phenomenon:

The "Layer 2 on fiat" framing is arguably the most technically accurate of these, because it captures both the dependency on the underlying fiat system and the increasingly autonomous behavior of the overlay network.

"Crypto trading itself is mostly redistribution of existing fiat between participants. The real macroeconomic effect comes from where the crypto originated, where it exits, whether it replaces national savings behavior, and whether it becomes dominant over local currency."

— The core insight that separates informed crypto economics from popular misconceptionSo, Does It Take Money Out of Sri Lanka?

Here is the honest, complete answer, because it depends entirely on which part of the ecosystem you are examining:

The local P2P trade itself does not drain national fiat reserves. What matters is the full journey: where did the USDT in circulation originally come from, and where does it ultimately go when it exits the crypto ecosystem?

If USDT circulates endlessly within Sri Lanka, bought, sold, traded, and held by Sri Lankans, the fiat anchor stays intact. The moment it exits to a foreign counterparty or is used to make an international payment, the equation changes.

Understanding this distinction is not merely academic. It is the foundation for thinking clearly about crypto policy, personal financial strategy, and the evolving role of stablecoins in developing economies like Sri Lanka's, where the informal crypto economy is already several years ahead of the regulatory framework trying to manage it.